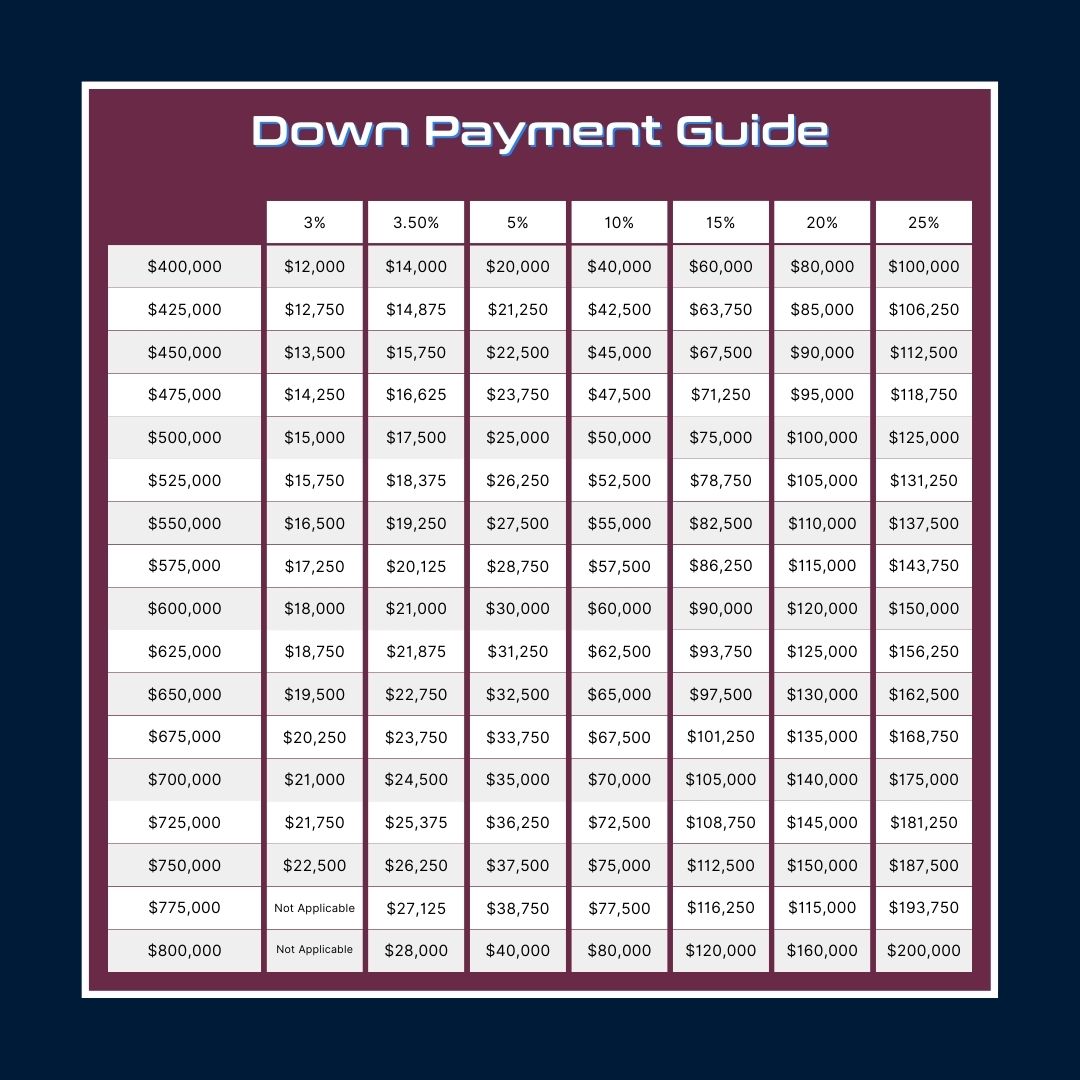

Pros and Cons of Different Down Payments: 0%, 3%, 5%, and 20% When Buying a Home

Buying a home is a significant financial decision, and one of the crucial factors to consider is the down payment. The down payment amount can vary, ranging from 0% to 20% of the home’s purchase price. Each down payment option has its own advantages and disadvantages, which potential homebuyers should carefully evaluate. In this article, we will explore the different implications of various down payment percentages to help you make an informed decision.

0% Down Payment: Advantages:

- Lower initial cost: A 0% down payment allows buyers to purchase a home without having to save for a down payment, making homeownership more accessible for individuals with limited savings.

- Immediate homeownership: By eliminating the need for a down payment, buyers can become homeowners quickly, which is beneficial for those seeking to move into a new home promptly.

Disadvantages:

- Higher loan amount: A 0% down payment means financing the entire purchase price of the home, resulting in a larger loan amount. This can lead to higher monthly mortgage payments and potentially more interest paid over the life of the loan.

- Mortgage insurance: Most lenders require borrowers with a 0% down payment to carry mortgage insurance, which protects the lender in case of default. This adds an additional cost to the monthly mortgage payment.

3% and 5% Down Payment: Advantages:

- Lower down payment: A 3% or 5% down payment still allows buyers to enter the housing market with a smaller upfront payment compared to a 20% down payment.

- More affordable upfront cost: With a smaller down payment, homebuyers can retain more of their savings for other expenses such as closing costs, moving, or home improvements.

Disadvantages:

- Higher monthly payments: A smaller down payment results in a larger loan amount, leading to higher monthly mortgage payments compared to a 20% down payment.

- Mortgage insurance: Similar to a 0% down payment, borrowers with a 3% or 5% down payment may be required to pay mortgage insurance, increasing the monthly payment further.

20% Down Payment: Advantages:

- Equity and lower loan amount: A 20% down payment allows buyers to immediately have equity in the home, reducing the loan amount and resulting in lower monthly mortgage payments.

- Avoiding mortgage insurance: With a 20% down payment, borrowers can typically avoid the additional cost of mortgage insurance, saving money in the long run.

Disadvantages:

- Higher upfront cost: Saving for a 20% down payment can be challenging, especially for first-time homebuyers. It may take longer to accumulate the necessary funds, delaying homeownership.

- Opportunity cost: While saving for a larger down payment, potential homebuyers miss out on potential price appreciation and the opportunity to start building equity sooner.

Choosing the right down payment amount when buying a home requires careful consideration. A 0% down payment offers immediate homeownership but comes with higher loan amounts and mortgage insurance costs. On the other hand, a 20% down payment provides lower monthly payments and helps avoid mortgage insurance but requires substantial upfront savings. The 3% and 5% down payment options strike a balance between affordability and loan size. Ultimately, homebuyers should assess their financial situation, weigh the pros and cons of each down payment percentage, and select the option that aligns with their long-term goals and financial capabilities.

Your lending team,

Jerry Torres I NMLS 365615

Yolanda Cordova I NMLS 1813699

LendiHome, Inc.